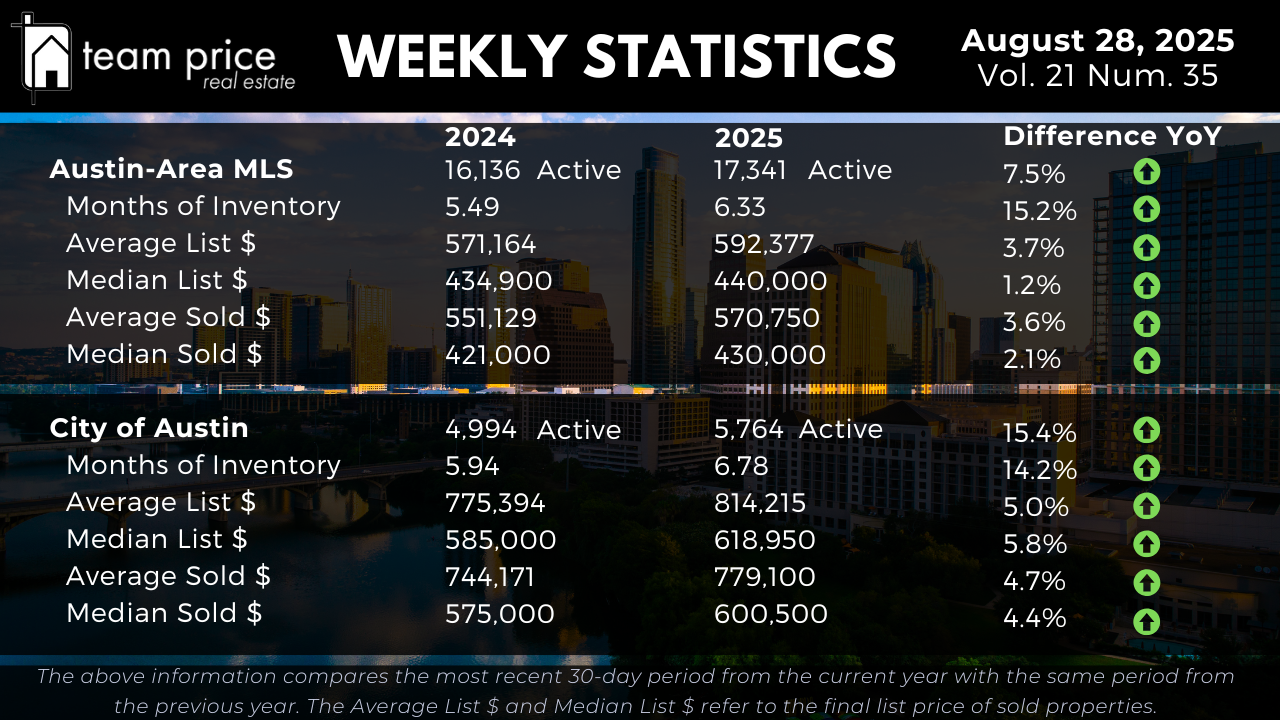

Inventory Expansion Across the Region

Active residential listings across the Austin-Area MLS reached 17,341 in August 2025, up 7.5 percent compared to 16,136 one year ago. Months of Inventory climbed from 5.49 to 6.33 months, representing a 15.2 percent increase. This expansion equates to 1.2 times more supply relative to the current pace of sales than last year. Inside the City of Austin, the increase is even sharper. Active listings rose 15.4 percent year over year, climbing from 4,994 to 5,764. Months of Inventory increased from 5.94 to 6.78 months, a 14.2 percent rise. Both measures indicate that buyers have more choices than they did a year ago, while sellers face more competition.

Pricing Trends in the Austin-Area MLS

Despite growing inventory, pricing trends remain positive compared to last year. The average list price for active homes in the Austin-Area MLS rose 3.7 percent to $592,377, while the median list price edged up 1.2 percent to $440,000. On the sales side, the average sold price increased 3.6 percent to $570,750, and the median sold price climbed 2.1 percent to $430,000. These gains show that although buyers are negotiating more aggressively, sellers are still achieving higher prices than they were in 2024. The data suggests a market that is cooling from its peaks but holding steady year over year.

Stronger Price Performance in the City of Austin

Within the City of Austin, pricing remains stronger than the regional average. The average list price advanced 5.0 percent year over year to $814,215, while the median list price rose 5.8 percent to $618,950. Closed sales confirmed this trend, with the average sold price climbing 4.7 percent to $779,100 and the median sold price rising 4.4 percent to $600,500. This performance highlights the resilience of Austin’s urban core, where sustained demand supports higher valuations even as inventory expands. Compared to the broader MLS, the city remains a relative outlier, showing more consistent appreciation across both active and sold prices.

Negotiation and Sold-to-List Ratios

Negotiation continues to define market behavior in 2025. So far this month, 69.27 percent of closed sales have occurred below list price, compared to 65.95 percent last month. The share of homes selling at list price dropped from 21.87 percent to 18.36 percent, while 12.37 percent sold above asking, virtually unchanged from July but below the 13.24 percent recorded in July 2024. The average sold-to-list price ratio stands at 96.85 percent, underscoring that most buyers are securing discounts. Sellers who set prices too aggressively risk longer market times and deeper concessions once negotiations begin.

Regional and ZIP Code-Level Insights

Conditions remain uneven across Central Texas, with variation between cities and ZIP codes. Of the 30 tracked cities, 53 percent reported month-over-month price increases while 47 percent recorded declines. On a year-over-year basis, 40 percent of cities posted gains while 60 percent experienced decreases. Importantly, none of the 30 cities are above their 12-month peak. At the ZIP code level, 51 percent of the 75 tracked areas reported monthly increases while 45 percent declined. Year over year, 47 percent posted gains while 53 percent showed losses. Only one ZIP code has exceeded its 12-month high, while 74 remain below their peaks. These results emphasize the importance of localized market knowledge, as performance varies considerably from neighborhood to neighborhood.

Prices Relative to Peak Levels

Even with recent gains, both the Austin-Area MLS and the City of Austin remain well below their historic peaks. In the broader MLS, the average list price is down 11.9 percent from its March 2023 high, and the median list price is 17.7 percent below its May 2022 peak. The average sold price is 12.9 percent below May 2022 levels, and the median sold price has dropped 18.6 percent. On a price-per-square-foot basis, values remain 21 to 24 percent below their highs. In the City of Austin, the numbers are slightly stronger but still reflect meaningful declines. The average list price is 13.8 percent below its April 2024 peak, and the median list price is 16.5 percent below its May 2022 high. The average sold price is down 8.8 percent from its May 2022 peak, and the median sold price has dropped 12.3 percent. Price-per-square-foot values in the city have fallen between 21 and 24 percent compared to 2022 highs.

Market Outlook

The Austin housing market at the end of August 2025 is best described as stabilizing. Inventory is higher, absorption has slowed, and buyers are negotiating more effectively, yet prices remain above last year’s levels. The region overall shows balance, while the City of Austin continues to demonstrate stronger pricing power. This balance creates a market environment defined by fundamentals rather than extremes. Buyers have more options and leverage, sellers must approach pricing with accuracy and discipline, and investors find opportunities in the gap between recent appreciation and declines from peak values. Austin real estate is no longer marked by rapid gains or sharp corrections but by a steady normalization toward long-term equilibrium.